Elasticity of demand measures how much the quantity demanded of a good responds to a change in its price. In simple terms, it tells us how sensitive consumers are to price changes.

-

Elastic demand: If the demand for a product changes significantly when the price changes, the product is said to have elastic demand. Consumers are sensitive to price changes. For example, if the price of a brand of chocolate increases, and people stop buying it or buy much less, the demand is elastic.

-

Inelastic demand: If the demand for a product doesn’t change much when the price changes, it has inelastic demand. Consumers are less sensitive to price changes. For example, basic necessities like salt or medicine usually have inelastic demand because people will still buy them even if the price goes up.

Types of Elasticity:

-

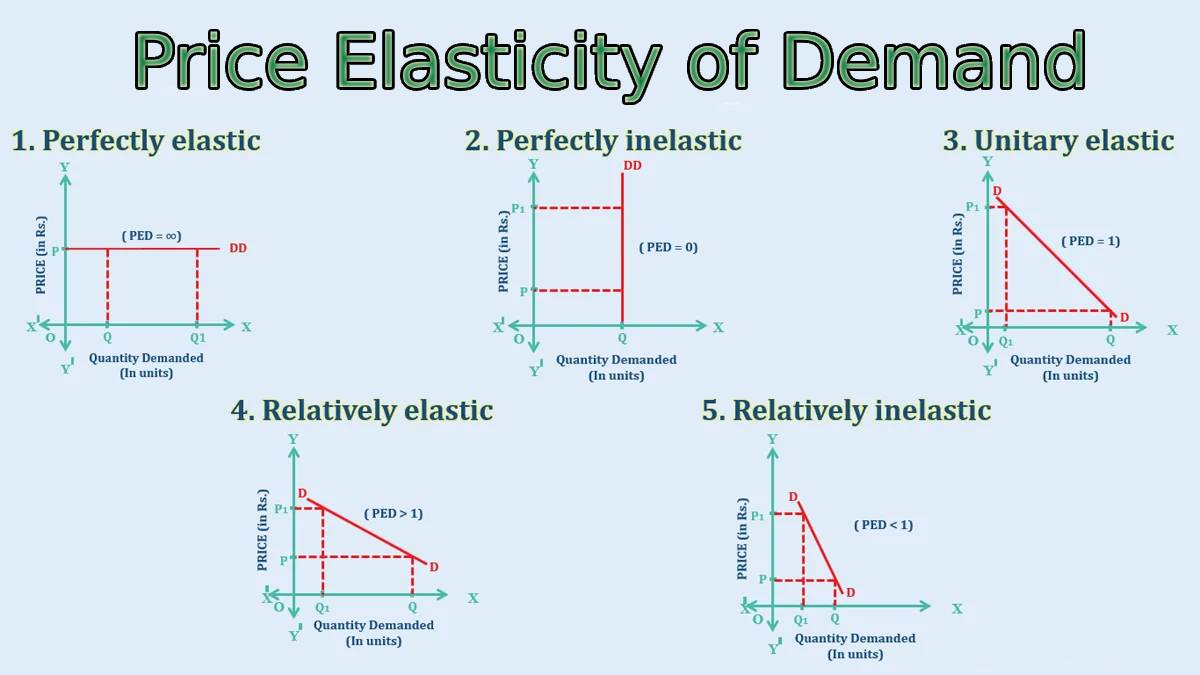

Price Elasticity of Demand (PED):

- This is the most common type of elasticity. It measures the responsiveness of quantity demanded to a change in the price of the good.

- Elastic Demand (PED > 1): A small change in price leads to a large change in quantity demanded.

- Inelastic Demand (PED < 1): A change in price leads to a small change in quantity demanded.

- Unitary Elastic Demand (PED = 1): The change in quantity demanded is exactly proportional to the change in price.

-

Income Elasticity of Demand (YED):

- This measures how the demand for a good changes as consumer income changes.

- Positive YED (Normal goods): If income increases, demand increases (e.g., luxury goods).

- Negative YED (Inferior goods): If income increases, demand decreases (e.g., cheaper brands).

-

Cross-Price Elasticity of Demand (XED):

- This measures how the demand for one good changes in response to a change in the price of another good.

-

- Positive XED (Substitutes): If the price of Good B rises, demand for Good A rises (e.g., if the price of tea rises, the demand for coffee might increase).

- Negative XED (Complements): If the price of Good B rises, demand for Good A falls (e.g., if the price of printers rises, the demand for ink cartridges may fall).

Summary of Elasticities:

- Elastic Demand: Consumers are very responsive to price changes. A small price change causes a relatively large change in demand.

- Perfectly Elastic Demand: Demand is infinitely sensitive to price changes. Even a small price increase causes demand to fall to zero.

- Inelastic Demand: Consumers are not very responsive to price changes. A price change leads to a smaller change in demand.

- Perfectly Inelastic Demand: Demand remains unchanged regardless of price changes. Price increases or decreases do not affect the quantity demanded at all.